SMM reported on July 9:

Metal market:

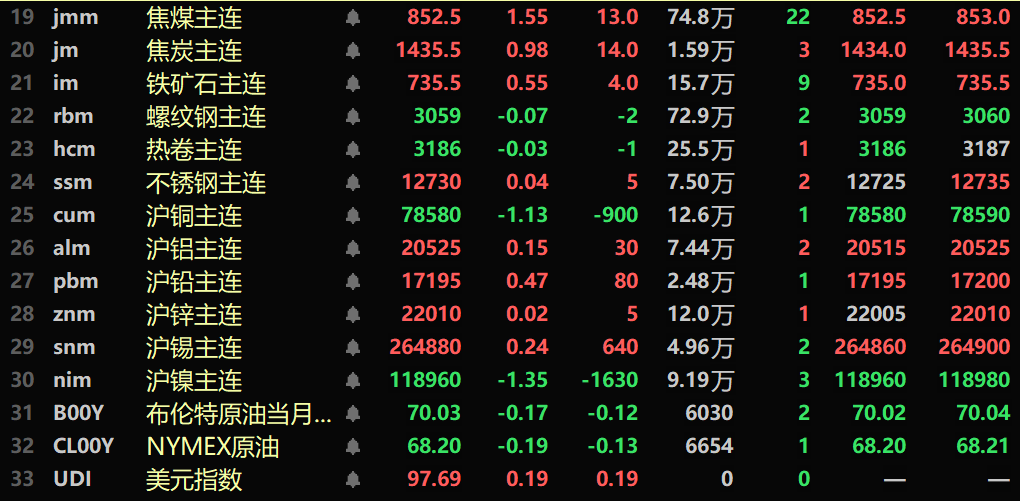

As of the midday close, domestic base metals generally rose, with SHFE copper down 1.13%, SHFE aluminum up 0.15%, and SHFE nickel down 1.35%. SHFE lead rose 0.47%, SHFE zinc saw a slight increase, and SHFE tin rose 0.24%.

Additionally, the main continuous futures contract for foundry aluminum rose 0.15%, and the main continuous contract for alumina rose 1.47%. Lithium carbonate rose 0.59%, while silicon metal fell 0.92%. Notably, the main continuous contract for polysilicon, which hit the daily price limit on the 8th, continued its upward trend from the previous five trading days, rising another 4.87%.

The ferrous metals series mostly rose, with iron ore up 0.55%, and rebar and HRC seeing slight declines. Stainless steel rose 0.04%. In the coking coal and coke sector: coking coal rose 1.55%, and coke rose 0.98%.

In the overseas metal market, as of 11:42, LME metals fell across the board, with LME aluminum down 0.48%, LME nickel down 0.51%, LME zinc down 0.4%, LME tin down 0.19%, LME lead down 0.56%, and LME copper down 1.21%. On the copper news front: According to multiple media outlets including CCTV, US President Trump stated on July 8 that he would impose a new 50% tariff on all copper imported into the US, but did not disclose the specific effective date of the new tariff. Trump said during a cabinet meeting at the White House that day: "I think we'll raise the tariff on copper to 50%." US Secretary of Commerce Lutnick also pointed out that day that the Commerce Department had completed its investigation into copper imports, and he expected the new tariff "to be implemented possibly by the end of July or August 1." (Financial Link)

In the precious metals sector, as of 11:42, COMEX gold fell 0.52%, and COMEX silver remained flat at $36.75/ounce; domestically, SHFE gold fell 0.97%, and SHFE silver fell 0.18%.

As of the midday close, the main continuous contract for the European container shipping index rose slightly by 0.05%, closing at 1980 points.

As of 11:42 on July 9, midday futures market conditions for some products:

》SMM Metal Spot Prices on July 9

Spot and Fundamentals

Copper:Today, the spot price of #1 copper cathode in Guangdong against the front-month contract ranged from a discount of 110 yuan/mt to a premium of 50 yuan/mt, with an average discount of 30 yuan/mt, up 20 yuan/mt from the previous trading day. SX-EW copper was quoted at a discount of 170 yuan/mt to a discount of 150 yuan/mt, with an average discount of 160 yuan/mt, down 10 yuan/mt from the previous trading day. The average price of #1 copper cathode in Guangdong was 79,180 yuan/mt, down 430 yuan/mt from the previous trading day, and the average price of SX-EW copper was 79,050 yuan/mt, down 440 yuan/mt from the previous trading day. Spot market: Guangdong's inventory continued to increase, marking the eighth consecutive day of increase... 》Click for details

Macro FrontZ16/>Domestic Updates:

[Zheng Shanjie: China's average economic growth rate reached 5.5% in first four years of 14th Five-Year Plan]Zheng Shanjie, Director of the National Development and Reform Commission (NDRC), stated at the State Council Information Office's press conference on "High-Quality Completion of the 14th Five-Year Plan" that China's average economic growth rate reached 5.5% in the first four years. Given the country's enormous economic scale and incremental growth, alongside shocks from the century-long pandemic and trade bullying, maintaining such growth momentum from this massive base is unprecedented in economic development history. China's economic expansion over the five-year period is projected to exceed 35 trillion yuan, equivalent to the combined 2024 GDP of Guangdong, Jiangsu, and Shandong (top three provincial economies), surpassing the total output of the Yangtze River Delta region and exceeding the GDP of the world's third-largest economy. The country contributes approximately 30% annually to global economic growth. Li Chunlin, NDRC Deputy Director, emphasized adhering to the principle of "moderately advanced but not excessive" infrastructure development, continuing to strengthen foundations, leverage advantages, address weaknesses, and enhance modern infrastructure systems. The 14th Five-Year Plan outlines 102 major projects, and after over four years of steady progress, significant advancements have been achieved with all target tasks expected to be completed by year-end. Zhou Haibing, NDRC Deputy Director, announced that China's NEV ownership reached 31.4 million units in 2024, marking a fivefold increase from 4.92 million units at the end of the 13th Five-Year Plan.》Click for details

[National Bureau of Statistics: June CPI shifted from decline to growth YoY while core CPI continued rebounding; PPI MoM decline unchanged from previous month]NBS data shows China's consumer price index (CPI) rose 0.1% YoY in June 2025, with urban areas up 0.1% and rural areas down 0.2%. Food prices declined 0.3%, non-food prices increased 0.1%, consumer goods prices fell 0.2%, and service prices rose 0.5%. H1 2025 CPI decreased 0.1% YoY. Month-on-month, CPI declined 0.1% in June, with urban areas down 0.1%, rural areas unchanged, food prices down 0.4%, non-food prices stable, consumer goods prices down 0.1%, and service prices flat. Dong Lijuan, Chief Statistician of NBS's Urban Survey Department, interpreted the June 2025 CPI and PPI data, noting the 0.1% CPI YoY increase marked a shift from four consecutive months of decline, primarily driven by the rebound in industrial consumer goods prices. The YoY decline in industrial consumer goods prices narrowed from 1.0% in the previous month to 0.5%, reducing the downward pull on CPI YoY by approximately 0.18 percentage points compared to the previous month. Core CPI rose 0.7% YoY, with the increase expanding by 0.1 percentage points from the previous month, reaching a new high in nearly 14 months. In June, PPI fell 0.4% MoM, the same decline as the previous month. The main reasons for the MoM decline in PPI are as follows: First, seasonal downward pressure on prices in some domestic raw material manufacturing sectors. Second, the increase in green electricity drove down energy prices. Third, prices in some industries with a relatively high share of exports came under pressure. 》Click for details

The central bank conducted 75.5 billion yuan of 7-day reverse repo operations today, with an operating interest rate of 1.40%, unchanged from the previous rate. As 98.5 billion yuan of 7-day reverse repo operations matured today, a net withdrawal of 23 billion yuan was realized.

US dollar:

As of 11:42, the US dollar index rose 0.19% to 97.69. The continued rebound in the US dollar index is mainly due to the retreat in market risk aversion sentiment, coupled with a slowdown in expectations for US Fed interest rate cuts, which supports the US dollar. The market continues to monitor changes in expectations for US Fed interest rate cuts. In addition, the market is paying attention to new developments in US tariffs and attempting to assess their impact. (Huitong Finance)

Data:

Today, the final value of the US May wholesale inventory monthly rate, the US July IPSOS Primary Consumer Sentiment Index (PCSI), the ANZ consumer confidence index for the week ending July 6 in Australia, and the official cash rate decision for July 9 in New Zealand, among others, will be released. In addition, the Reserve Bank of New Zealand (RBNZ) will announce its interest rate decision and monetary policy assessment report, and RBNZ Governor Orr will hold a monetary policy press conference.

Crude oil:

Both oil futures fell. As of 11:42, US oil fell 0.19% and Brent oil fell 0.17%. Although tariffs have raised concerns about damage to oil demand, strong travel demand over the July 4 weekend has brought hope to the market. Data from the American Automobile Association (AAA) last week showed that a record 72.2 million Americans are expected to travel more than 50 miles (approximately 80 kilometers) during the Independence Day holiday.

The US Energy Information Administration (EIA) forecast in a monthly report on Tuesday that US oil production in 2025 will be lower than previously expected due to falling oil prices prompting US producers to slow down production activities this year. The EIA expects US oil production to be 13.37 million barrels per day in 2025, down from the previous forecast of 13.42 million barrels per day; it expects production to be 13.37 million barrels per day in 2026, unchanged from the previous forecast.

Additionally, the market expects OPEC oil-producing countries to approve another significant production increase in September, which would complete the reversal of voluntary production cuts by eight member states and allow the UAE to raise output under a higher production quota. Separately, the latest data released by the American Petroleum Institute (API) showed a rise in US crude oil inventories last week, while distillate and gasoline inventories declined. For the week ending July 4, crude oil inventories increased by 7.13 million barrels, gasoline inventories fell by 2.18 million barrels, and distillate inventories dropped by 830,000 barrels. (Webstock Inc.)

Spot Market Overview:

►Shanghai Zinc: Premiums adjusted lower WoW, spot market transactions weakened [SMM Midday Review]

Other metal spot market midday reviews will be updated shortly—please refresh to view~